A Familiar Name for Belfast Readers

If you live in Belfast, there is a good chance you have encountered Reach plc without ever noticing the company behind it.

One of their digital properties is Belfast Live, which has quietly become one of the most widely read local news sites in the city. The same group also owns national titles such as the Daily Mirror, Daily Express, and Daily Star, along with dozens of regional newspapers across the UK.

Most readers encounter these brands individually. Investors have to step back and look at the system that sits behind them.

That system turns attention into advertising revenue. For decades it did so at enormous scale.

The difficulty today is that the industry which once produced those cash flows is slowly shrinking.

Understanding Reach therefore requires separating two different forces that sit inside the same company:

- the economic engine that still produces cash

- the legacy obligations that absorb much of that cash

Once those two pieces are visible, the economics of the business become much easier to reason about.

The Business in Plain English

At its core, Reach produces news and entertainment content and distributes it through a portfolio of media brands.

The content itself is fairly ordinary: news, sport, opinion pieces, lifestyle coverage, and entertainment stories written by editorial teams across the country.

That content reaches readers through several channels:

- printed newspapers

- digital news websites

- mobile applications

- social platforms and search engines

The economic logic of the business is simple.

Reach produces content that attracts readers.

Readers create attention.

Advertisers pay to reach that attention.

In other words, Reach is fundamentally an audience aggregation business.

For most of the past century that audience was monetised through newspapers. Today it increasingly sits on websites.

The transition between those two worlds is where the interesting economics lie.

Two Businesses Living Inside One Company

Reach today effectively operates with two revenue engines that behave quite differently.

Print still forms the backbone of the business.

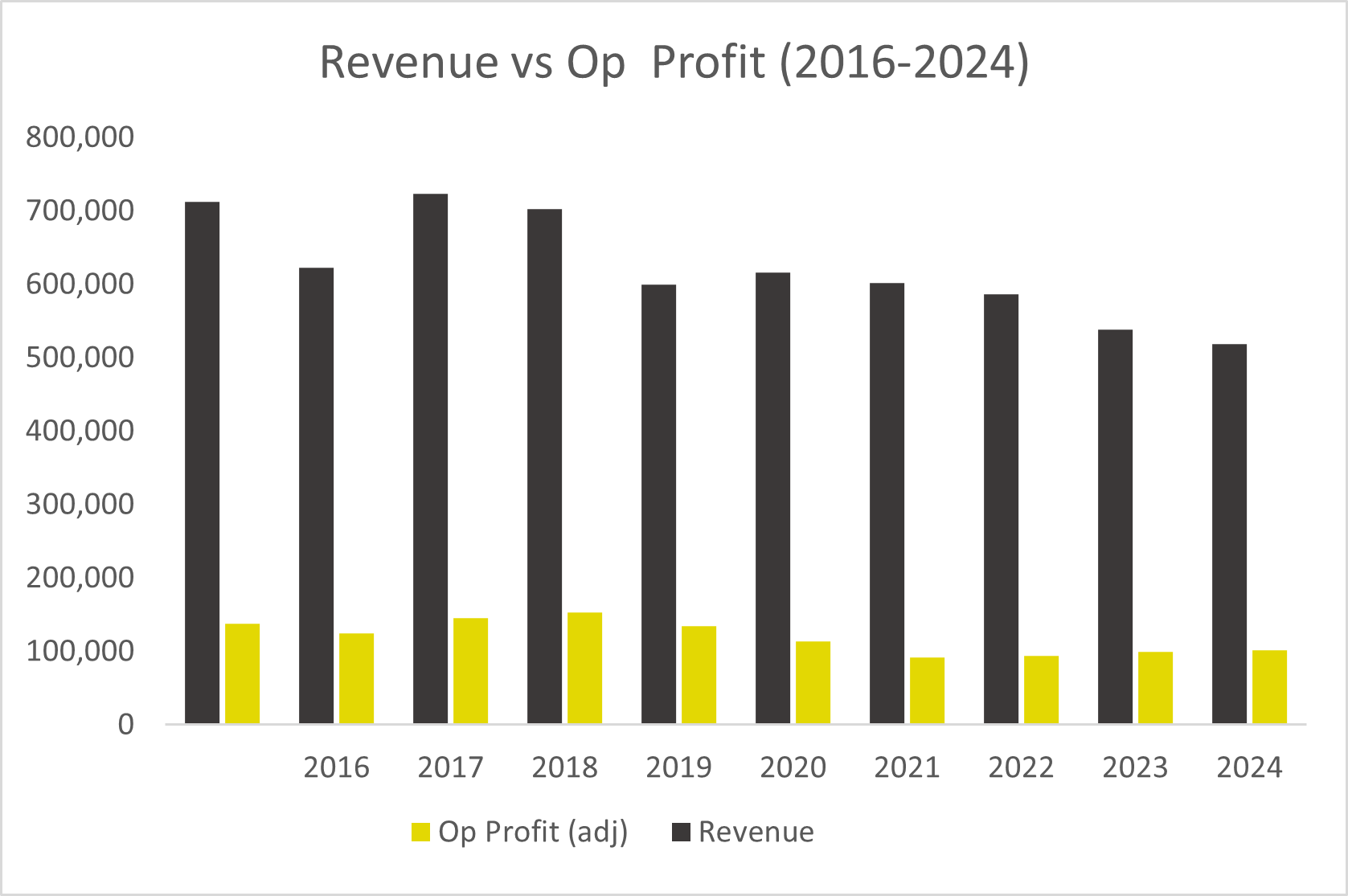

Despite years of decline, it continues to generate roughly three quarters of group revenue, with digital accounting for the remaining quarter.

Circulation continues to fall, but the remaining readership tends to be older and remarkably loyal. That loyalty allows the company to raise cover prices over time, which helps offset falling volumes.

For investors this matters because print behaves like a declining but still profitable asset.

Digital

Digital is the long-term replacement engine.

Reach’s websites collectively attract millions of readers each day, and those audiences are monetised primarily through advertising.

Digital revenue depends largely on two variables:

- traffic volumes

- revenue per thousand page views (RPM)

Traffic itself is heavily influenced by platforms such as Google and social media networks that direct readers toward Reach’s sites.

The result is a business where digital reach is large, but pricing power is weaker than it once was in print.

Print generates the cash today.

Digital determines what the business might look like tomorrow.

Looking at the Cash Engine

When I started looking at Reach, the first step was to rebuild the cash flow structure from the company’s reports rather than relying on summary numbers from financial websites.

That exercise revealed a useful three-layer framework.

Layer 1 – Operating Cash Flow

The operating engine of the business still generates substantial cash.

Adjusted operating cash flow sits at roughly:

£100 million per year

This represents the cash produced by the publishing operation before investment or legacy obligations.

Layer 2 – Core Free Cash Flow

Once maintenance capital expenditure is deducted, we arrive at the cash available to the business as a whole.

Capex has been running at roughly £13–14 million per year, leaving something close to:

£85–90 million of core free cash flow

At this level the business actually looks very cash generative.

But this still is not the cash that ultimately reaches shareholders.

Revenue and operating profit have both declined over time, but operating margins have remained relatively resilient.

Simplified cash flow structure

Core operating FCF: ~£90m

Structural obligations: ~£20mNormalised equity FCF: ~£70m

Current pension deficit payments temporarily absorb much of this cash,

with contributions expected to fall significantly after 2027.

The Part Most Investors Miss

The gap between core free cash flow and equity cash flow is where Reach becomes interesting.

Large pension obligations and other legacy commitments absorb a significant share of the operating cash flow.

Defined benefit pension schemes were built during decades when the newspaper industry was far more profitable than it is today.

The newspapers declined.

The pension promises remained.

Many legacy media companies carry the same burden.

In practical terms this means that a large portion of the cash generated by the operating business is redirected toward pension deficit payments rather than shareholders.

The operating engine continues to produce cash.

The balance sheet determines how much of that cash investors ultimately receive.

Modelling the Cash Harvest

To understand how these forces interact over time, I built a simplified cash harvest model.

The goal was not to predict the future precisely, but to explore how the economics evolve under a set of reasonable assumptions.

Model assumptions (approx.)

Revenue decline: ~4% per year

Operating margin: ~19%

Capex intensity: ~2.6% of revenue

Discount rate: ~10%

Terminal growth: -2%

Under those assumptions the operating business itself appears to be worth roughly:

£350 million in enterprise value

But enterprise value is not what equity holders receive.

Once the model accounts for net debt and the present value of pension obligations, the implied equity value falls to roughly:

£170 million

With approximately 320 million shares outstanding, that translates to something in the region of:

£0.50–£0.60 per share

Interestingly, that is broadly in line with where the market has recently priced the stock.

What the Market Appears to Believe

Viewed this way, the market valuation begins to make more sense.

The current price seems to reflect a fairly conservative view of the future. Revenue continues declining, the pension deficit absorbs much of the operating cash flow, and the business gradually winds down rather than stabilising.

Under those conditions the present valuation is not obviously irrational.

But the model also highlights how sensitive the outcome is to relatively small changes in assumptions.

If the decline remains moderate and the pension burden eventually stabilises, the company may be able to return a substantial portion of its current market value to shareholders over time.

In situations like this the outcome often depends on something simpler than a dramatic turnaround. The business does not need to succeed spectacularly. It only needs to decline more slowly than the market expects.

There are also small developments within the business that could matter at the margin. Digital formats such as video, podcasts, and other platform-native content continue to expand across the group’s titles. None of these individually transform the economics of the company, but they have the potential to gradually improve digital monetisation over time.

In a business already generating significant cash, even modest improvements can shift the balance between decline and value extraction.

The Real Question

The investment case does not hinge on whether Reach becomes a growth company again.

That seems unlikely.

The real question is simpler.

Can the business continue generating meaningful cash while the legacy obligations gradually fade?

That does not require heroics.

It simply requires the business to keep doing what it already does.

Produce content.

Attract audiences.

Sell advertising.

Harvest the remaining economics of a declining industry.

Sometimes the market prices a business as though the lights are about to go out.

Occasionally the lights just dim slowly.

Model

A simplified version of the valuation model used in this article is available below.